✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🧠 Sound smart? Feed your brain with weekly issues sent directly to your inbox here

Today’s Bullets:

- What’s a Debt Jubilee?

- Examples of Jubilees

- Not (really) possible for the US Treasury

- So, then what?

Inspirational Tweet:

If you didn’t see this past week, The White House cancelled up to $10K of student loans for any borrower making under $125K per year, as well as other loans. This led to a lot of people asking why he didn’t just cancel all student debt or more. In fact, wWhy not just cancel all debt, including US Treasuries the Fed already owns?

Well, while that would be great for the Treasury’s deficit problem, it would effectively ‘break’ the Fed’s balance sheet.

How?

Let’s walk through it nice and easy, as always, shall we?

🥳 What’s a Debt Jubilee?

In the simplest form, a debt jubilee is when large organization or country cancels a large amount of debt. In other words, it forgives the borrower(s) from responsibility to pay back the loans they have assumed.

Debt jubilees can come in many shapes, forms, and sizes, though they are often enacted by governments who see them as a way to avoid deep economic recessions or a depression. Of course, they can also be used to ‘redistribute’ wealth amongst a population that is experiencing a separation between its wealthiest and poorest echelons.

The most recent debt jubilee we’ve seen came from the White House forgiving federal issued student loans this past week. This forgiveness is estimated to add up to nearly $330B over ten years, and was touted as a way to help indebted students who are struggling to make payments as we emerge from the pandemic. Many, however, see the move as a political stunt, meant to ‘buy votes’ ahead of an important cycle of mid-term elections.

Whatever the reason, the reality is this: a type of debt jubilee like this one simply moves the debt from consumers’ balance sheets and places it right onto the government’s.

How?

Students owe the federal government borrowed money to pay for tuition in the form of subsidized loans from the government. When the government forgives these, they essentially remove an asset from the Treasury’s balance sheet (when someone owes you money, it is a liability on their balance sheet and an asset on yours). The money the government was counting on receiving from students is wiped out and it causes lower expected revenue. Since the US government already (and perpetually) operates in a deficit, it will need to resort to additional borrowing to make up the difference.

How?

Issue more Treasuries, and borrow the money to make up the difference.

tuition money loaned to students → students owe government through loans → government forgives loans → government must borrow more to replace revenue

So, The government has simply moved the loans from the student’s balance sheet onto their own. Which has many people criticizing the jubilee and yet others asking, why stop there? Why not just reset the balance sheet and forgive it all. Credit cards, mortgages, all the student debt. Put it all on the government’s balance sheet. Let them borrow the money.

This would help close the wealth gap, right?

Well, maybe temporarily, but if you’ve been reading The Informationist, then you’re well aware of the debt problems we’re currently facing across the globe and even here in the US. And how this debt problem is exacerbating the need for high inflation as a way to wipe away past debt by paying it off with cheaper future dollars. And as assets and homes and rents and food increase in price, inflation, only creates a larger separation of wealth for a country or region.

If you have not read the latest issue of the newsletter, I highly recommend taking a few moments to check it out. You can find it right here.

Back to jubilees.

Bottom line, with debt to GDP in the US over 137%, the US government is in no position to take on the burden of additional debt they just did, no less trillions more in the form of a consumer debt jubilee.

Still, with a growing separation of wealth in many developed countries, it is easy to see why some citizens of these regions are calling for large scale debt jubilees to reduce all debts and solve the issue.

It has, of course, been done many times before.

🤑 Examples of Jubilees

Debt jubilees have been around for over 4,000 years and can be traced back to ancient Babylon, where kings would use them as regular resets to redistribute wealth among classes.

In ancient Israel, debt jubilees were decreed to occur every fifty years, allowing people to go back to the land they were forced to turn over to creditors because of their debts. Additionally, any Hebrew that had taken another Hebrew as an indentured servant, was to cancel the servant’s debts and free him the Jubilee Year.

Of course we’ve also seen debt jubilees in the modern world, most notably in 1948, when the Allied Powers replaced the Germany’s Reichsmark with the Deutsche mark, wiped out 90% of its government and private debt, which allowed Germany to emerge as nearly debt-free and with affordable production costs, and this sparked its Economic Miracle.

And then most recently, in 2008, the Iceland government assumed and wrote off massive amounts of mortgage debt of its citizens, during the Great Financial Crisis.

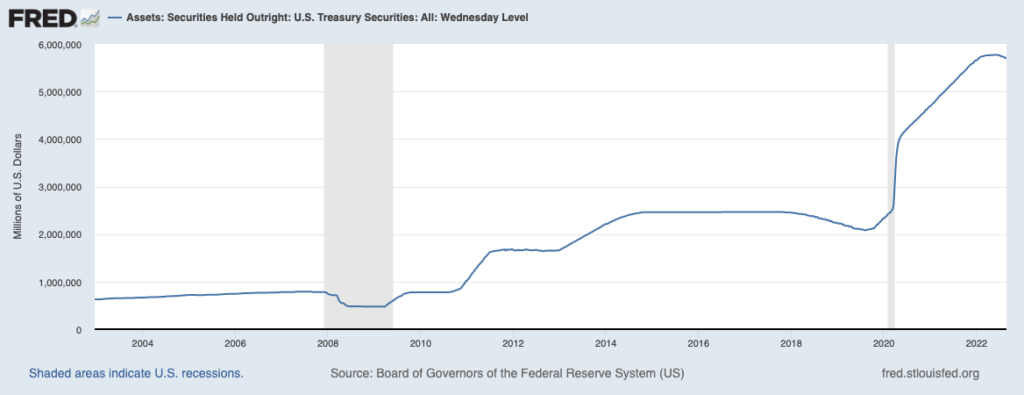

But today, we have a bit of a new phenomenon with central banks of countries printing money and buying their own debt. Some countries are even the largest owners of their own debt. The Bank of Japan, for instance, owns over 50% of all Japanese issued government debt. The US central bank, The Federal Reserve, owns over $5.7T of its own government’s issued US Treasuries.

These are dollars one hand of the government has effectively borrowed from its other hand. So, why not just press a button and wipe those hands clean of all this ghost debt?

🧐 Not (really) possible for the US Treasury

Well, technically, the US could do this with the mere press of a button, as they say. But if we did, then we would not only create a balance sheet issue, but we would officially enter the circus realm of governing and effectively wipe out the remaining confidence foreign nations have in US Treasuries as a reserve asset.

Let’s take a peek at the current balance sheet of the Fed to understand better.

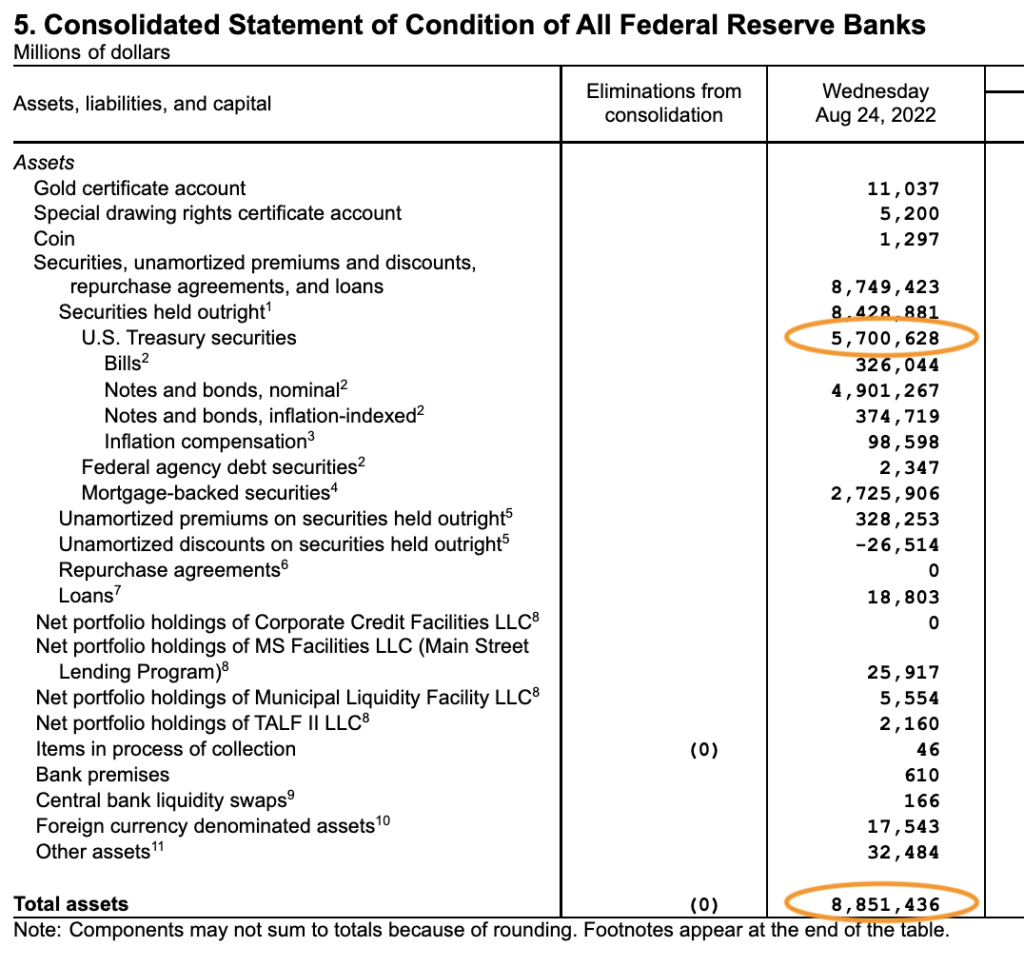

Looking at the most recent Consolidated Statement of Assets published by the Fed, we see the US Treasury Securities listed that match the chart of $5.7T above.

We also see that the Total Assets the Fed lists on its balance sheet to be $8.85T.

Not to get too technical here, but basic accounting requires your total listed Assets to match your total listed Liabilities + Capital. If these don’t match, then something is incorrect in your accounting and your books cannot be certified as accurate or trustworthy.

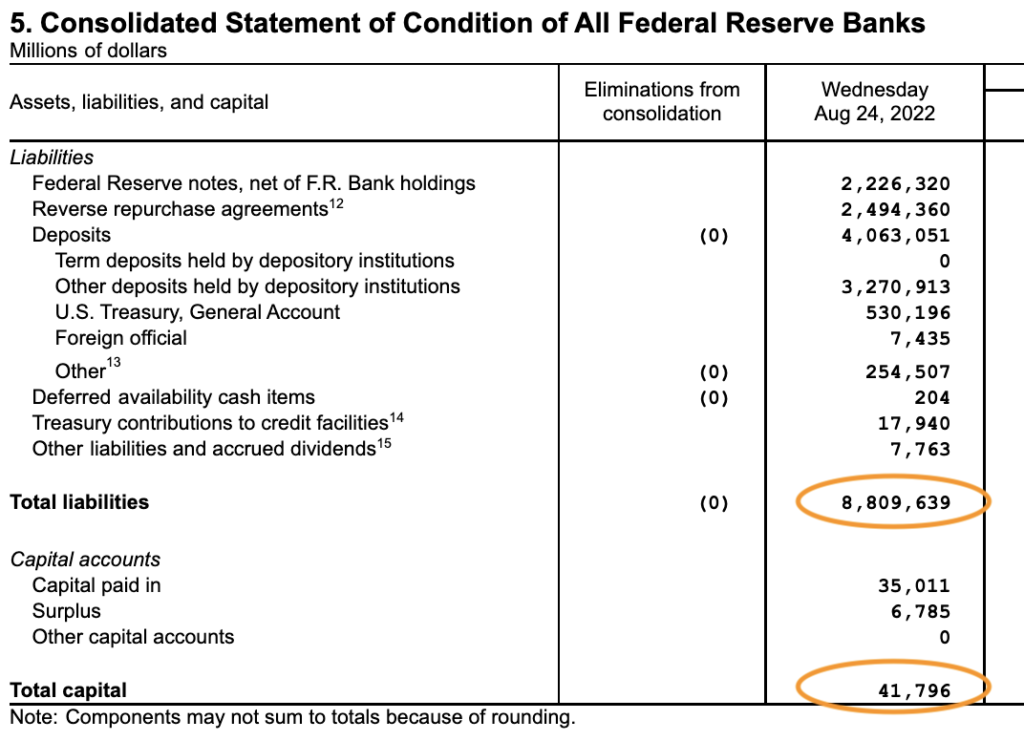

So, let’s then take a look at the Fed’s Consolidated Statement of Liabilities and Capital.

OK, $8.809T of liabilities plus $41.79B capital equals $8.85T. Our assets match our liabilities/capital.

And all those Deposits and Reverse Repurchase Agreements are basically cash that is being stored at the Fed by commercial banks. In other words, that cash in circulation is being collateralized by all the debt on the Fed’s balance sheet.

So, what happens if we wipe out the $5.7T of US Treasury assets above?

Well, this leaves us with a massive hole in our balance sheet that can only be reconciled by creating a negative capital balance. We would effectively be left with $3.15T in assets and $8.85T in liabilities.

The Fed would be insolvent.

The only way to solve this, really, would be for the US Treasury to press another button to print an equal amount, $5.7T, of cash and deposit that at the Fed to create a new asset to offset the cash liability.

Can you say, Clown Republic?

This will not happen here. At least not yet. 🙄

🤨 So, then what?

Okay then, if we can’t just issue a debt jubilee to wipe out all this debt, then what’s the alternative? How can we stave off the debt spiral for as long as possible and avoid a collapse of our credit system from the sheer load of debt that is expanding at an increasing rate annually?

I have one word for you.

Inflation.

That’s right. As the dollar devalues with inflation, the bonds debase with the repayment of those debts. In other words, inflation erodes the purchasing power of a bond’s future cash flows.

And in even simpler terms:

If I borrow $100 from you today and promise to repay you in ten years, with inflation, the $100 I repay you is not worth as much as it was when I borrowed it. I.e., $100 today may buy 25 cups of coffee. In ten years, $100 may only buy you five or ten cups. I am paying you back with cheaper dollars.

As the creditor, you lose.

And this is exactly what the government is doing with its bonds. It’s the only game they can effectively play for a long time without having to completely reset the counter and re-price the USD across all assets.

And so what’s your personal recourse? How can you protect yourself from the inflation?

Or more importantly, the exponential expansion of the USD money supply?

Well, in my opinion, it has become critically important to buy and hold scarce assets and hard money in order to participate in the constant devaluing of the USD. As the USD deflates, assets inflate and you are protected.

I’m personally diversified into equities, real estate, gold and silver, and as you may have heard me say before, I believe the asset that will beat all of these in the future is Bitcoin.

That’s it. I hope you feel a little bit smarter knowing about debt jubilees and how we are quite unlikely to ever seen one for US Treasuries.

Before leaving, feel free to respond to this newsletter with questions or future topics of interest. And if you want daily financial insights and commentary, you can always find me on Twitter!

✌️Talk soon,

James